Although the net method is theoretically better, it seems to be less efficient than recording vendor invoices at their stated amounts. If Big Guitar, LLC was unable to pay the invoice by January 11, it would have to reverse the discount taken and record the actual payment. Money is constantly needed by businesses to run their daily operations, service financing costs and undertake any growth plans. Several vendors offer their customers a cash discount as an incentive to make timely payments. However, the total profit reported over time will be the same under both methods as long as the physical flow of goods and the actual payment terms are the same.

Do you already work with a financial advisor?

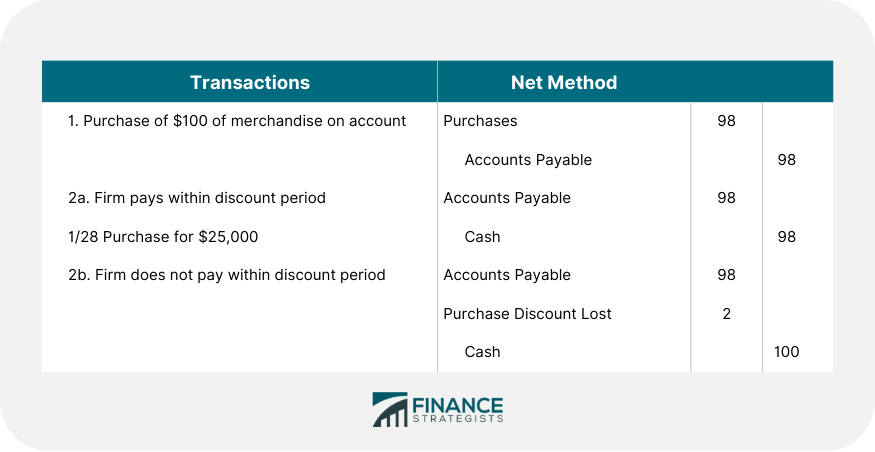

However, in the net method, we record the purchase transaction at the net amount assuming that the payment would be made exactly on or before the agreed credit term. In this method, the amount of purchase recorded is the amount of invoice minus the cash discount. Your gross revenue amount gives an overview of income, which helps to plan for large-scale cost management.

Amount at which sales are recorded

From a financial perspective, purchase discounts are cost-effective ways for businesses to move stock quickly and maintain a healthy profit margin. There are two types of purchase discounts and the accounting treatment for these two discounts is different from one and another. When looking at an income statement, you can usually find net revenue listed below gross revenue. Calculating turbotax news and articles and tracking your net revenue gives you a better understanding of your company’s profitability. This additional cost represents a cost for the use of money and therefore is considered interest. The Gross Method helps to provide accurate financial information by making sure payment amounts reflect reality, rather than showing inflated sales figures or artificially lowered expenses.

- You can use gross and net revenue during financial planning to make smart decisions, set achievable goals, and ensure long-term business success.

- When a business sells a product, it needs to know if it is making money, and employees need to know how their pay is calculated.

- In this method, the amount of purchase recorded is the amount of invoice minus the cash discount.

- To calculate the sale price of an item, subtract the discount from the original price.

- By capturing the total value of sales and purchases, businesses can better track their financial activities and understand the true scale of their operations.

Get the latest insights from thousands of sales professionals.

Some may post the charge as an offset to the expense, as an offset to a payable, or as an income item. Under gross method, there is no impact on accounting if cash discount is not availed. In this lesson you’ll learn about pro-forma financial statements and how to estimate specific line items on the balance sheet, income statement, and statement of cash flows. Under gross method, sales are recorded at full invoice value without considering discount.

The Accounts Payable account is credited when goods or services are purchased on credit terms . The accumulated depreciation account is an asset account with a credit balance ; this means that it appears on the balance sheet as a reduction from the gross amount of fixed assets reported. When a company uses its payroll it is formulating a system to distribute paychecks to its employees for the hours worked in the week. Learn more about payroll cost calculations, its definitions, gross pay, overtime and how to calculate net pay. If the buyer uses the perpetual inventory method, there would be no “Purchases”, “Purchase Discount”, and “Purchase Discount Lost” accounts.

Thus at the end of each month, the cost accountants can compare billings to customers against shipping paid. Shipping paid or freight out is NOT part of cost of goods sold, but rather is considered a selling expense. Under gross method, the discount entry will be recorded and an expense will be debited. Gross method is considered as a more accurate and complete way of recording credit sales as it follows the complete transaction flow. Under gross method, the sales are recorded at full value and hence income is recorded at a higher value initially. The purchase accounts are used along with freight in, and the beginning and ending inventory to determine the cost of goods sold (COGS).

Since at the time of sale, it is not possible to know whether the customer will actually avail the discount, therefore Company A would choose either gross method or net method. Once one of the methods is selected, all sales must be recorded according to that method for consistency. The basic way to calculate a discount is to multiply the original price by the decimal form of the percentage. To calculate the sale price of an item, subtract the discount from the original price.

Accounts payable are recorded at their expected cash payment at the time of purchase. The argument for treating discounts lost as interest expense is based on the fact that the firm consciously chose not to pay within the allowable discount period, thus causing an additional cost. If the payment is made within the discount period, Accounts Payable should be debited, and Cash should be credited for the amount at which the payable was originally recorded. This month’s order totals $10,000, but Bob’s supplier offers discount terms of 2/10, n/30.

Examining all aspects and looking at both the long-term results and short-term gains before deciding which course of action to take will provide the most clarity when it comes time to make a decision. FOB specifies which party (buyer or seller) pays for which shipment and loading costs and where responsibility for the goods is transferred. The last distinction is important for determining liability for goods lost or damaged in transit from the seller to the buyer.

Cash discounts may be recorded in the books of the company using the gross method or the net method. Under the gross method, sales and purchases are initially recorded at gross amount and when the discount is taken, “Sales Discount” or “Purchase Discount” is recorded. A cash discount is a deduction allowed by the seller of goods or by the provider of services in order to motivate the customer to pay within a specified time. As noted above, expenses are almost always debited, so we debit Wages Expense, increasing its account balance. Since your company did not yet pay its employees, the Cash account is not credited, instead, the credit is recorded in the liability account Wages Payable. Purchase discount is an offer from the supplier to the purchaser, to reduce the payment amount if the payment is made within a certain period of time.

However, under the net method, we need to record adjusting entries to recognize the loss of the discount. Acas provide free and impartial advice to employers and workers on employment matters. A business that offers cash discounts on credit sales can use the gross method to account for those sale. Under this method, you do not assume your customer will take advantage of your discount offer.